That frustrating feeling when your credit score plateaus, despite making all your payments on time, often stems from a single overlooked number: your credit utilization ratio. Think of it as the silent gatekeeper between you and premium interest rates, higher credit limits, and loan approvals. A “Credit to Debt Calculator” (also known as a Credit Utilization Calculator) is the essential tool that demystifies this critical metric, giving you the power to understand, manage, and master your revolving credit usage.

What is a Credit to Debt (Utilization) Calculator?

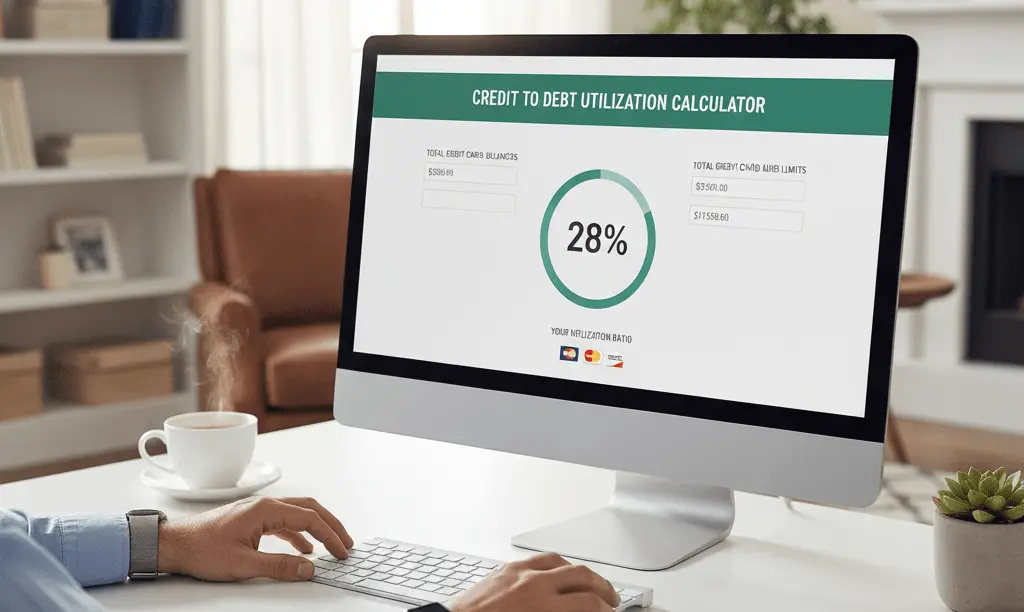

At its core, a Credit to Debt Calculator is a specialized tool designed to measure the health of your revolving credit. It takes the fundamental snapshot that lenders use to assess risk: how much of your available credit you are actually using.

The Core Formula

The calculation is elegantly simple, yet its impact is profound:

For example, if you owe $2,500 across all your cards and have a combined credit limit of $10,000, your utilization is 25%.

Credit-to-Debt vs. Debt-to-Income: The Crucial Difference

A common point of confusion is conflating this with Debt-to-Income (DTI). It’s vital to understand the distinction:

- Credit-to-Debt (Utilization) Ratio: This measures your revolving credit balances against your revolving credit limits. It’s a key factor in your FICO score (30%).

- Debt-to-Income (DTI) Ratio: This measures your total monthly debt payments against your gross monthly income. It’s a key factor for loan qualification (especially mortgages).

In short: Utilization is for your credit score. DTI is for your loan application. A good calculator focuses on the former.

How Does the Calculator Help You Manage Your Credit Like a Pro?

A sophisticated calculator does more than basic math. It transforms raw numbers into an actionable credit strategy.

1. Visualizing the “Danger Zone” in Real Time

The best calculators instantly highlight when you cross critical thresholds. While you may know you have “some debt,” seeing your ratio jump from 29% to 35% and turn red makes the risk tangible. The 30% mark is a well-established industry benchmark; exceeding it can trigger significant score drops. A good calculator makes this boundary impossible to ignore.

2. Enabling Powerful Scenario Planning

This is where the real magic happens. A pro-level calculator allows you to play “what if” with your finances.

- Question: “If I put my $1,000 tax refund toward my cards, how much will my score improve?”

- Calculator Action: Input a hypothetical $1,000 payment. It instantly recalculates, showing your new utilization percentage—for example, dropping from 45% to 32%.

- Result: You see a direct, quantifiable link between a financial action and a credit outcome, empowering smarter decisions.

3. Identifying High-Risk Cards with Precision

Your overall ratio is critical, but FICO also scrutinizes per-card utilization. A card at 95% of its limit is a massive red flag, even if your overall number looks okay. An advanced calculator breaks down utilization for each card, answering the strategic question: “Should I pay off the card with the smallest balance or the one that’s maxed out?” The data-driven answer is almost always to attack the highest-ratio card first for the fastest score boost.

Why Your “Utilization Ratio” is the Secret to a High Score

Understanding the “why” behind the number is key to motivation.

- Beyond the 30% Rule: While staying below 30% helps you avoid penalties, it’s not the goal for an elite score. Consumers with scores above 780 consistently maintain utilization in the single digits. For the absolute best rates, your target should be under 10%, with 1-5% being the optimal “sweet spot.”

- The Lender’s Perspective: To a bank, high utilization doesn’t just mean you have debt; it signals that you might be financially overstretched and relying on credit to cover everyday expenses. This makes you a higher-risk borrower. A low ratio demonstrates restraint, control, and ample financial breathing room.

Strategies to Improve Your Ratio (Using Your Calculator Results)

Armed with your calculator’s insights, you can execute targeted strategies.

1. The “Micropayment” or “Mid-Cycle Payment” Strategy:

Don’t wait for your statement. Your credit card issuer typically reports your balance to the bureaus once a month on your statement closing date. Use your calculator to determine a target balance. Then, make a payment a few days before this date to ensure a low balance is reported. This simple timing trick can dramatically lower your reported utilization without changing your actual spending.

2. The Strategic Limit Increase Request:

This is a powerful mathematical fix. If you get your credit limit increased from $5,000 to $7,500 while keeping your balance at $1,000, your utilization drops from 20% to 13% overnight. Use your calculator first to model different limit scenarios and see the impact. Crucial Warning: This only works if you don’t increase your spending alongside your limit.

3. The “Avalanche” Method for Utilization:

While the debt “snowball” method (paying smallest balances first) has psychological benefits, for pure credit score optimization, the “avalanche” method targeted at high utilization is superior. Use your calculator to identify the card with the highest individual utilization percentage and focus your payments there first. This directly targets what’s hurting your score the most.

Conclusion: Your Roadmap to a Healthier Score

A Credit to Debt Calculator isn’t just an arithmetic tool; it’s a financial diagnostic and strategic planning system. It turns the vague anxiety of “I have too much credit card debt” into a clear, percentage-based problem with a defined solution path. It answers the critical questions: How bad is it? What’s the fastest fix? What will this payment actually do?

Stop guessing about your credit health. The path to a higher score starts with understanding the numbers that control it.

Ready to take control? Grab your latest credit card statements. Add up your total balances and total credit limits. See where you stand—then use a precise calculator to build your plan to get to 10% and below.